Under Gramm-Leach-Bliley

The United States found itself at the onset of the 21st century without Glass-Steagall to guide its banking practices. In many ways, this was not a big jump from where they had been on the other side of the 2000 line since the legislation had been severely whittled down by bank lobbyists and economic conservatives in the twenty years preceding.

2004 saw the five-year anniversary of Gramm-Leach-Blilely. The Federal Reserve observed little change in those five years, with banking practices running largely as they had in the 1990s. Citigroup Inc. gave up property and casualty underwriting when it spun off Travelers in 2002, and after selling their life insurance business in 2005, were operating on terms that would have still been legal under Glass-Steagall. This was mostly done to prevent Traveler's property and causality insurances from dragging down Citigroups' market worth because the then recent 9/11 terrorist attacks had made the services Traveler's offered much more vulnerable. Many understood these developments to mean that the liberal fear of banking conglomerates forming rampantly under GLBA was unfounded. This claim was heavily supported by the Fed Reserve Board and was stated in their 2003 Joint Report to Congress.

Despite the sense that Gramm-Leach-Bliley hadn't caused much if any harm, the early 2000s were riddled with corporate scandals. Commercial banks were getting more involved in dealing securities, which may have inflated stock prices, or at least given mega-companies like Enron and WorldCom the incentive to raise their share values by any means necessary. Both companies falsified accounting records to trick investors into thinking their companies were doing far better than they actually were. It was discovered that these frauds began in the mid-1990s after Glass-Steagall had already been dealt debilitating damage. WorldCom also owned UUNET at the time,which was one of the largest early internet service providers. While the internet was certainly on a huge upswing through the 90s and 2000s, UUNET exaggerated these numbers, creating speculation in telecommunication, and contributing to the dot-com bubble crash.

The United States found itself at the onset of the 21st century without Glass-Steagall to guide its banking practices. In many ways, this was not a big jump from where they had been on the other side of the 2000 line since the legislation had been severely whittled down by bank lobbyists and economic conservatives in the twenty years preceding.

2004 saw the five-year anniversary of Gramm-Leach-Blilely. The Federal Reserve observed little change in those five years, with banking practices running largely as they had in the 1990s. Citigroup Inc. gave up property and casualty underwriting when it spun off Travelers in 2002, and after selling their life insurance business in 2005, were operating on terms that would have still been legal under Glass-Steagall. This was mostly done to prevent Traveler's property and causality insurances from dragging down Citigroups' market worth because the then recent 9/11 terrorist attacks had made the services Traveler's offered much more vulnerable. Many understood these developments to mean that the liberal fear of banking conglomerates forming rampantly under GLBA was unfounded. This claim was heavily supported by the Fed Reserve Board and was stated in their 2003 Joint Report to Congress.

Despite the sense that Gramm-Leach-Bliley hadn't caused much if any harm, the early 2000s were riddled with corporate scandals. Commercial banks were getting more involved in dealing securities, which may have inflated stock prices, or at least given mega-companies like Enron and WorldCom the incentive to raise their share values by any means necessary. Both companies falsified accounting records to trick investors into thinking their companies were doing far better than they actually were. It was discovered that these frauds began in the mid-1990s after Glass-Steagall had already been dealt debilitating damage. WorldCom also owned UUNET at the time,which was one of the largest early internet service providers. While the internet was certainly on a huge upswing through the 90s and 2000s, UUNET exaggerated these numbers, creating speculation in telecommunication, and contributing to the dot-com bubble crash.

Subprime Mortgage Crisis

Enter the age of subprime lending. Simply put, giving huge loans to people who have little to no chance in hell or any other ideological-arena of ever paying them back.

A lot of this risky lending was done by a new economic player, shadow banks. While Gramm-Leach-Bliley significantly broke down banking regulations, shadow banks were able to shy under the radar and avoid almost any regulation. Shadow bank is a blanket term for a financial institution that is like a bank, but isn't. Confusing? That's the point. What they essentially do is borrow lots of short-term funds and reinvest in long-term assets. But because they are technically not banks, they are not supervised or insured by the FDIC.

Shadow banks jumped to economists' attention because of their growing involvement with the housing market, using their special brand of finance alchemy to turn home mortgages into securities. A bunch of mortgages would be packaged up together and used as collateral for stocks that were then sold to investors, but these were very risky investments because many of the mortgages that backed the stock (securities) were of subprime borrowers. Then it just became a game of non-disclosure hot potato hoping you weren't stuck with the mortgages when the homes were foreclosed making you take on all the losses.

Enter the age of subprime lending. Simply put, giving huge loans to people who have little to no chance in hell or any other ideological-arena of ever paying them back.

A lot of this risky lending was done by a new economic player, shadow banks. While Gramm-Leach-Bliley significantly broke down banking regulations, shadow banks were able to shy under the radar and avoid almost any regulation. Shadow bank is a blanket term for a financial institution that is like a bank, but isn't. Confusing? That's the point. What they essentially do is borrow lots of short-term funds and reinvest in long-term assets. But because they are technically not banks, they are not supervised or insured by the FDIC.

Shadow banks jumped to economists' attention because of their growing involvement with the housing market, using their special brand of finance alchemy to turn home mortgages into securities. A bunch of mortgages would be packaged up together and used as collateral for stocks that were then sold to investors, but these were very risky investments because many of the mortgages that backed the stock (securities) were of subprime borrowers. Then it just became a game of non-disclosure hot potato hoping you weren't stuck with the mortgages when the homes were foreclosed making you take on all the losses.

|

|

It would be one thing if shadow banks were entirely separate from regular banks, but many of these shadows were owned and controlled by legitimate banks. Beyond that, the financial markets that both dealt in were so intertwined that trouble for one meant trouble for the other. In short, banks and non-banks engaged in subprime lending, giving adjustable rate mortgages (ARMs) to people with little means of paying them back. This was done through predatory lending practices that purposely misled millions of Americans without the finance suave of big banks and investors. These mortgages were resold to investors to back stocks as mortgage-backed securities bundled into collateralized debt obligations (CDOs). Because so many homes were being sold, it created a speculative bubble in the housing industry. But when subprime borrowers began defaulting on their loan payments, their homes were foreclosed and their mortgages plummeted in value.

|

So all the credit that people borrowed from the banks couldn't be repaid, meaning all the credit banks had borrowed from the Federal Reserve at the low interest rate set by Alan Greenspan could also not be repaid. Now the homeowners with their mortgages and the banks and investors with their CDOs have all gone bankrupt and so begins a massive recession.

Too Big To Fail

Nearly 80 years after the Stock Market Crash, the 2008 Global Financial Crisis put the world through its worst economic trouble since the Great Depression. By September of 2008, Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation) had over $5 trillion in mortgage obligations, while national mortgage debt was at over $10.5 trillion. This spurred the federal takeover of Fannie Mae and Freddie Mac, putting them under conservatorship. Many powerful financial institutions were on the brink of collapse while stocks fell globally. The housing market was a mess, and foreclosures, evictions, and repossessions were common jointed with rising unemployment. Liquidity, which is an asset's ability to rapidly change into cash, became nearly impossible and money stopped flowing through the economy as people saved up what little they still could.

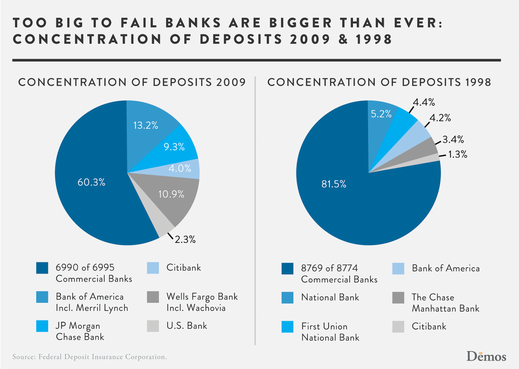

While millions of Americans suffered in debt, the biggest five banks in the U.S. were so indebted by fraudulent credit that by the end of 2007, their debt totaled $4.1 trillion, accounting for over 30% of the nominal GDP. To understand how significant that is, all of American industry only accounts for less than 20% so only five banks were together making more than 1.5 times the blanket of U.S. industrial businesses. These big banks were so big, essentially forming the crux of the U.S. economy that if they fell, the rest of the economy would as well.

Big banks knew they were so big that the government couldn't let them go under, which encouraged their risky practices with the knowledge that they'd be saved if things didn't go well. To them it was like playing a video game with infinite lives, they didn't need to be cautious. They were operating under the safety net of Too Big To Fail, a theory that says that some institutions are so central to the health of the economy that they should receive aid if they are starting to sink. However fiscal policies are set to benefit and save these enormous institutions, which they can use to their advantage and profit seek off of by using added leverage that would otherwise be too risky.

Nearly 80 years after the Stock Market Crash, the 2008 Global Financial Crisis put the world through its worst economic trouble since the Great Depression. By September of 2008, Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation) had over $5 trillion in mortgage obligations, while national mortgage debt was at over $10.5 trillion. This spurred the federal takeover of Fannie Mae and Freddie Mac, putting them under conservatorship. Many powerful financial institutions were on the brink of collapse while stocks fell globally. The housing market was a mess, and foreclosures, evictions, and repossessions were common jointed with rising unemployment. Liquidity, which is an asset's ability to rapidly change into cash, became nearly impossible and money stopped flowing through the economy as people saved up what little they still could.

While millions of Americans suffered in debt, the biggest five banks in the U.S. were so indebted by fraudulent credit that by the end of 2007, their debt totaled $4.1 trillion, accounting for over 30% of the nominal GDP. To understand how significant that is, all of American industry only accounts for less than 20% so only five banks were together making more than 1.5 times the blanket of U.S. industrial businesses. These big banks were so big, essentially forming the crux of the U.S. economy that if they fell, the rest of the economy would as well.

Big banks knew they were so big that the government couldn't let them go under, which encouraged their risky practices with the knowledge that they'd be saved if things didn't go well. To them it was like playing a video game with infinite lives, they didn't need to be cautious. They were operating under the safety net of Too Big To Fail, a theory that says that some institutions are so central to the health of the economy that they should receive aid if they are starting to sink. However fiscal policies are set to benefit and save these enormous institutions, which they can use to their advantage and profit seek off of by using added leverage that would otherwise be too risky.

So banks and shadow banks engage in subprime lending which eventually leads to a market collapse and bankruptcies everywhere, but if the big banks fail, then things get even worse. There seems to be no answer to this conundrum but the one that appeared was bailouts. Quite simply, the government would just give money to these failing industries until they could stay afloat. Meanwhile all the people who had fallen victim to these banking schemes were out of luck, and for many, out of a home. To make things even less fair, it was the people and their tax dollars that bailed out the banks and financial institutions that had taken them for fools in the first place.

Obama signing the Dodd Frank Act

Obama signing the Dodd Frank Act

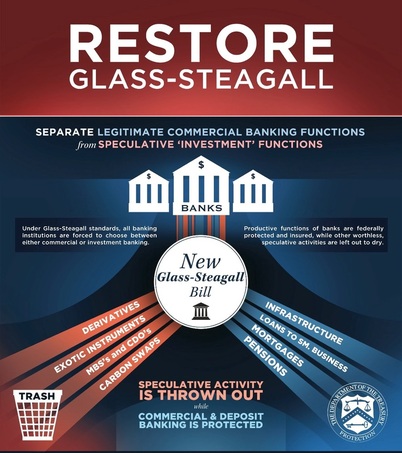

Restoring Glass-Steagall

Whether the repeal of Glass-Steagall was a significant cause of the Global Recession remains to be debated. There are many economic experts who say it did have a role while others still insist it didn't. Either way, its repeal marked a financial cultural shift that encouraged reckless risk-taking. Even banks themselves are beginning to realize how dangerous it is that they've become so big and advocating for banks to be broken up into smaller institutions. Sandy Weill, the former director of Citigroup and vanguard leader in the repeal of Glass-Steagall turned about-face and declared in a 2012 interview that Glass-Steagall contributed to nearly 50 crisis-free years and needs to be brought back.

In light of the false-credit fueled recession, there have been several efforts to try and restore some version of Glass-Steagall to varying degrees of success. The Obama administration has not helped with this restoration process and President Obama has publicly stated that he does not believe that Gramm-Leach-Bliley or Glass-Steagall deregulation caused the financial crisis and opposes the act being restored.

In 2009 Rep. Maurice Hinchey tried amending the Dodd-Frank Wall Street Reform and Consumer Protection to include reenacting Glass-Steagall sections 20 and 32, both dealing with Federal Reserve System banks relation to security-trading firms:

Section 20 prevented any (deposit) banks from affiliating with security-trading firms

Section 32 prohibited commercial bank officers and directors from advising these firms

In the end, the amendment was never voted on by the House.

Later that same year, Senators Maria Cantwell and John McCain introduced the Banking Integrity Act of 2009, which would also reenact sections 20 and 42, but this was also not voted on, this time by Senate. April of 2011 saw the introduction of the Return to Prudent Banking Act of 2011 but it was not acted on before the 112th Congress left session.

Whether the repeal of Glass-Steagall was a significant cause of the Global Recession remains to be debated. There are many economic experts who say it did have a role while others still insist it didn't. Either way, its repeal marked a financial cultural shift that encouraged reckless risk-taking. Even banks themselves are beginning to realize how dangerous it is that they've become so big and advocating for banks to be broken up into smaller institutions. Sandy Weill, the former director of Citigroup and vanguard leader in the repeal of Glass-Steagall turned about-face and declared in a 2012 interview that Glass-Steagall contributed to nearly 50 crisis-free years and needs to be brought back.

In light of the false-credit fueled recession, there have been several efforts to try and restore some version of Glass-Steagall to varying degrees of success. The Obama administration has not helped with this restoration process and President Obama has publicly stated that he does not believe that Gramm-Leach-Bliley or Glass-Steagall deregulation caused the financial crisis and opposes the act being restored.

In 2009 Rep. Maurice Hinchey tried amending the Dodd-Frank Wall Street Reform and Consumer Protection to include reenacting Glass-Steagall sections 20 and 32, both dealing with Federal Reserve System banks relation to security-trading firms:

Section 20 prevented any (deposit) banks from affiliating with security-trading firms

Section 32 prohibited commercial bank officers and directors from advising these firms

In the end, the amendment was never voted on by the House.

Later that same year, Senators Maria Cantwell and John McCain introduced the Banking Integrity Act of 2009, which would also reenact sections 20 and 42, but this was also not voted on, this time by Senate. April of 2011 saw the introduction of the Return to Prudent Banking Act of 2011 but it was not acted on before the 112th Congress left session.

The closest that we currently have to the Glass-Steagall act is the Volcker Rule which was included as part of the Dodd-Frank Act in 2010. This watered down Glass-Steagall stand-in prevents FDIC commercial banks and their affiliates from involving themselves with hedge funds and private equity funds. It also prohibits propriety trading which causes speculation by investing the bank's own funds to pick economic winners to invest in to make a heightened profit.

However, the Volcker Rule plainly gives banks the go-ahead to trade U.S. government-issued obligations like Fannie Mae or Freddie Mac bonds. And although investment and commercial banking are essentially separated, a hazy line is reestablished in allowing market-making, helping put sellers and buyers of securities together. More gray areas are set up by allowing banks to hedge to reduce risk under the argument that it is necessary for bank's solvency. Hedging essentially allows banks to bet on black and red by investing in a way so that if one of their portfolios tanks, it will cause another portfolio to make back some of that money. This is highly problematic because hedging for big institutions dips into the convoluted realms of PhD math and guesswork and/or voodoo trickery as far as the rest of us non-economic-mathematics-wizards know. But still the biggest problem with the Volcker Rule is that although it was passed and was meant to be implemented by the end of July, 2012, this has not happened and the rule is still not currently in effect.

The strongest modern movement to restore Glass-Steagall is led by Senator Elizabeth Warren, along with Senators Cantwell, McCain, and Angus King. They propose the 21st Century Glass-Steagall Act which is still highly contested. Unlike many previous attempts at restoration, this 21st Century Glass-Steagall Act would not try to bring back sections 20 and 32 of the original act. In essence this 21st century revision would address the separation of savings/checking account banks from riskier activities which would in turn cause large institutions to break down and take away the security of bailout from those that remained. If this push for standard regulation ends up by the wayside it will beg the question of how many more financial crises the American people will have to shoulder before financial policy is finally modernized.

However, the Volcker Rule plainly gives banks the go-ahead to trade U.S. government-issued obligations like Fannie Mae or Freddie Mac bonds. And although investment and commercial banking are essentially separated, a hazy line is reestablished in allowing market-making, helping put sellers and buyers of securities together. More gray areas are set up by allowing banks to hedge to reduce risk under the argument that it is necessary for bank's solvency. Hedging essentially allows banks to bet on black and red by investing in a way so that if one of their portfolios tanks, it will cause another portfolio to make back some of that money. This is highly problematic because hedging for big institutions dips into the convoluted realms of PhD math and guesswork and/or voodoo trickery as far as the rest of us non-economic-mathematics-wizards know. But still the biggest problem with the Volcker Rule is that although it was passed and was meant to be implemented by the end of July, 2012, this has not happened and the rule is still not currently in effect.

The strongest modern movement to restore Glass-Steagall is led by Senator Elizabeth Warren, along with Senators Cantwell, McCain, and Angus King. They propose the 21st Century Glass-Steagall Act which is still highly contested. Unlike many previous attempts at restoration, this 21st Century Glass-Steagall Act would not try to bring back sections 20 and 32 of the original act. In essence this 21st century revision would address the separation of savings/checking account banks from riskier activities which would in turn cause large institutions to break down and take away the security of bailout from those that remained. If this push for standard regulation ends up by the wayside it will beg the question of how many more financial crises the American people will have to shoulder before financial policy is finally modernized.